In today’s private lending landscape, terms like white labeling, correspondent lending, and table funding are often flung around interchangeably, but their distinctions matter deeply. For private lenders aiming to scale, expand product offerings, or preserve brand identity, understanding these models is essential. This article breaks down each approach, highlighting the legal, operational, and strategic implications for private lending professionals.

White Labeling

White labeling is nearly identical to wholesale lending. The loan originator doesn’t use its own funds; instead, they broker the loan to a third-party funding source. Unlike wholesale arrangements, however, the borrower believes the originator is also tied to the funding source, even though they are not, thanks to a generic entity name like “Funding Lender LLC” used on loan documents.

Documentation & Disclosure

- The funding party controls loan documentation and is the actual named lender—but often under a generic alias to obscure its identity.

- Loan originators may receive payment after closing, without directly showing compensation on the settlement statement.

Legal & Practical Considerations

- This approach can raise misrepresentation risks if borrowers believe the originator is funding the loan.

- Funding sources typically require the originator to provide representations and warranties, including proof of licensing in states in which an originator must be licensed to originate business purpose loans.

- A trusted third-party such as Fortra Law may handle closings to preserve anonymity of the actual funder.

Summary: White labeling can elevate an originators brand and expand their product suite without requiring the originator to separately source capital for these deals. But to execute it cleanly, both originator and funding source must be thoughtful about administrative details such as what e-mail signatures are used throughout the transaction, which parties are identified on any settlement statement and other details to ensure regulatory compliance and ease of transacting for all parties involved.

Table Funding

Table funding shares similarities with white labeling: the originator appears to fund the loan, but capital comes from a third party. The distinguishing factor is that the originator is explicitly named as the lender in loan documents, followed by a contemporaneous assignment of the mortgage and Note at the closing table, assigning the loan from the originator to the funding source.

Documentation Flow

- The originator is on the loan documents as the lender.

- At closing, funds are delivered by the true funder, and an assignment of the mortgage is filed immediately.

Legal & Licensing Aspects

- Gives the appearance of direct lending without the misrepresentation risk of white labeling, as the assignment is transparent post-closing.

- May require careful handling of insurance and title policies, ensuring the true funder is properly insured or named as typically the named lender (here the originator) is often the insured party for title and hazard insurance purposes.

- Licensing rules vary—California, for example, prohibits table funding altogether, while other states may offer licensing advantages if the originator is named as lender which is the case in Michigan for example.

Pros & Cons

Table funding at scale is very difficult to accomplish because of the coordination required. Typically originators and funding lenders will choose to use table funding only with deep trust between originator and funder—usually limited to strong TPO relationships.

Gives originators brand leverage—being named as lender is powerful. The originator IS the lender in the borrower’s eyes.

Operationally complex: requires careful coordination for assignments and post-closing quality control. The funding party must be certain the Assignment closed contemporaneously with the Mortgage and that the funding party is named for all insurance policies.

Correspondent Lending

In the correspondent lending model, the originator funds the loan with its own capital but intends to sell the loan shortly thereafter to another lender, who may have more robust capital or secondary market access. For anyone who has originated a consumer conventional mortgage loan, they almost certainly have done this through a correspondent lending arrangement. The originator IS the funding source, however, the originator intends on offloading the loan off its balance sheet as fast as possible to a loan buyer.

Underwriting & Documentation

- Two underwriting paths:

1) Non‑delegated underwriting: The loan buyer handles underwriting and guarantees purchase.

2) Delegated underwriting: The originator underwrites according to buyer’s guidelines but carries risk if the buyer declines to purchase leaving the originator with the risk of holding on its own balance sheet indefinitely, or often selling the loan at a discount, particularly if there are any perceived defects during loan origination such as the failure to properly identify signatories or even simple typos. - Originator is named as lender initially, followed by assignment to loan buyer typically 3-30 days later.

Legal Framework

- Licensing similar to direct lending; originator must meet regulatory requirements for funding loans.

Strengths & Weaknesses

- Offers immediate funding flexibility for originators but requires upfront capital.

- Earns revenue through “gain on sale”—premium over par when loan is sold, particularly for DSCR loans.

- Typically allows originator retain all origination related fee income rather than splitting this income between originator and funding party which is what occurs in white label or table fund situations, typically.

- Risk exposure: if underwriting fails or documentation is flawed, the loan buyer may reject purchase or otherwise demand a discount on the loan.

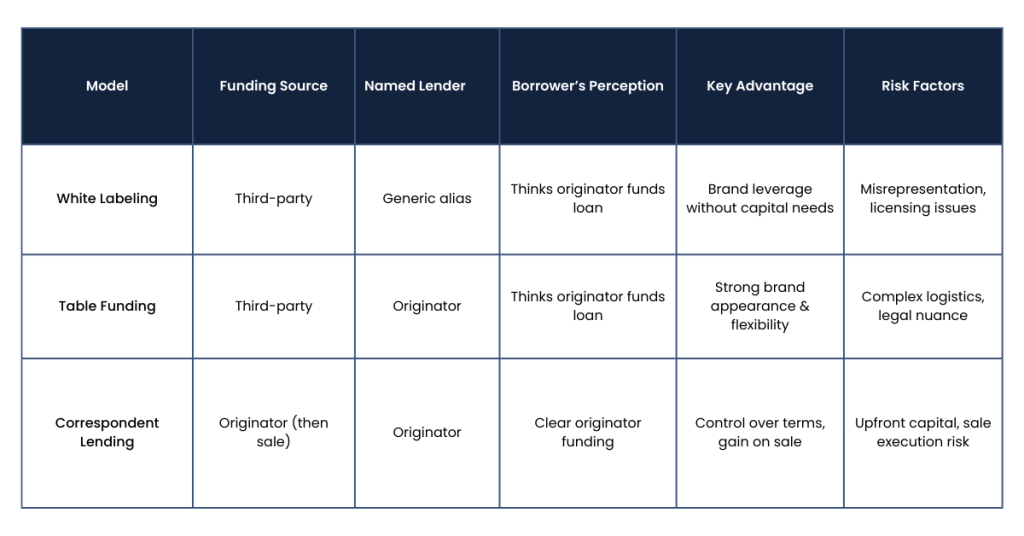

At a Glance: Comparative Table

Strategic Takeaways for Private Lenders

Evaluate Your Capital Position

- No capital or want to preserve liquidity? White labeling shines.

- Want brand dominance? Table funding is ideal assuming the funding source can offer.

- Able to fund and sell? Correspondent lending offers profit potential via “gain on sale.” and allows the originator to maintain maximum control of the borrower/originator relationship.

Understand Your Licensing Environment

- Table funding may simplify licensing in some states; while it is strictly prohibited in others (e.g., California).

- Clear contractual relationships are vital in white labeling to protect against misrepresentation claims.

Weigh Operational Complexity

- White labeling and table funding rely heavily on process clarity, often involving legal intermediaries for closings.

- Correspondent lending requires underwriting alignment with buyers and documentation precision.

Foster Trust with Partners

- Table funding typically works best with deeply trusted originators you can rely on to handle assignment and closing mechanics smoothly.

- Correspondent lending hinges on accurate underwriting to ensure the buyer’s confidence in loan performance.

How Fortra Law Can Help

For private lenders, the choice between white labeling, table funding, and correspondent lending hinges on strategy, capital availability, licensing jurisdictions, and brand ambitions. Understanding each model’s mechanics, legal implications, and operational demands empowers you to scale effectively while preserving borrower trust and compliance integrity.

At Fortra Law, we advise the nation’s largest private lending institutions on all of the strategies outlined above. Contact us today to learn more.

For lenders interested in a deeper dive, you can access our free recorded webinar, co-hosted with Forta Law Partner Melissa Martorella, Esq., over on YouTube. This hour-long webinar provides a comprehensive breakdown of all the lending models discussed above, with a Q&A session at the end.